Bitcoin has spent fifteen years proving one thing better than any asset on earth. It settles value with absolute reliability. It does not bend, inflate, or break. It has become the world’s most secure Settlement Layer and the foundation for a global store of value. What it has not become is a productive asset. That is the void Bitcoin DATs are trying to fill. They take Bitcoin on the balance sheet and build a capital allocation machine around one goal, compounding BTC per share.

But this category is not one model and it is not one quality bar. Some DATs are built to compound BTC per share through cycles with disciplined financing and transparent custody. Others are little more than dilution wrappers with a Bitcoin narrative attached. The difference shows up in one place: whether the structure can earn trust when the market turns.

What are Bitcoin DATs?

A Bitcoin DAT (Digital Asset Treasury) is a company that is normally listed, whose treasury strategy is to hold Bitcoin as a core reserve asset on its balance sheet and to use corporate finance tools (equity issuance, converts, secured debt, operating cash flow) to increase BTC per share over time, rather than simply hold BTC passively.

MSCI and other index providers are starting to formalise the category. One definition classifies a Digital Asset Treasury Company as a listed firm where digital asset holdings are 50% or more of total assets, capturing the Bitcoin balance sheet model.

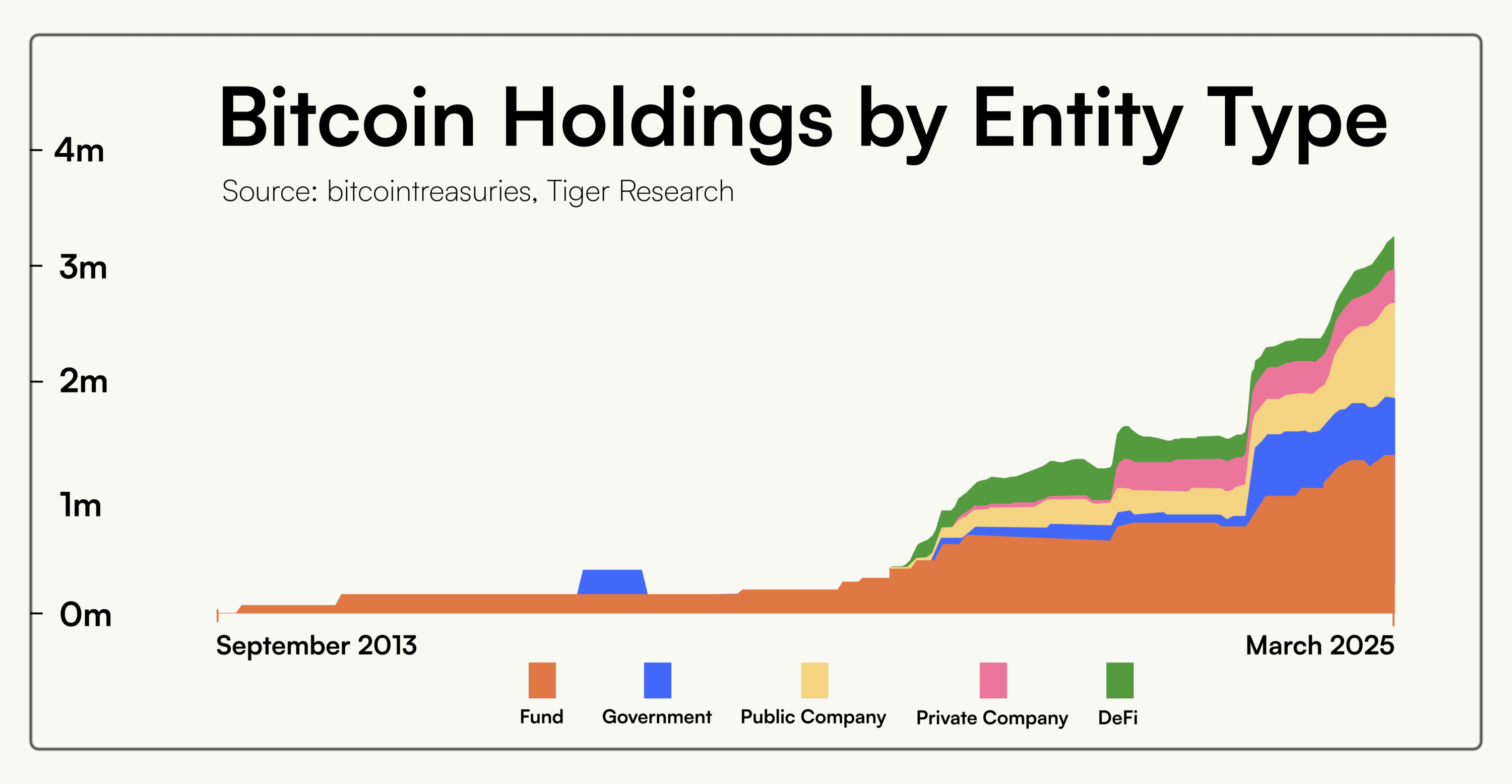

Data shows there are 361 public companies currently holding BTC. Holdings are now meaningful at the system level:

- Public Companies: 1,094,050 BTC

- Private Companies: 288,315 BTC

- Government Entities: 647,032 BTC

- ETFs and Exchanges: 1,642,950 BTC

- DeFi and Other: 376,744 BTC

That is roughly 5.5% of Bitcoin supply, second only to ETFs and exchanges. Five years ago this was niche. Today it is a defined category with hundreds of entities. With current growth, a plausible end state may be that a material share of BTC sits within some form of DAT.

A Bitcoin DAT is not a spot ETF. It is not designed to track NAV tightly. It has discretion. It can raise equity, issue converts, or borrow against assets, and it can trade at a premium or discount to the value of the Bitcoin it holds. That flexibility is the opportunity and the risk. Done well, the structure compounds BTC per share through disciplined financing and transparent custody. Done badly, it becomes a dilution and leverage wrapper that only works while market sentiment does.

What they are trying to achieve

The original goal

Bitcoin DATs began as a straightforward balance sheet decision. Hold Bitcoin as a core treasury reserve so the company is positioned for debasement risk and long duration upside. Most DATs entered the category for one or both of the following reasons.

Ideological hedge against fiat debasement

Management believes structural currency dilution makes cash a melting ice cube. Holding BTC is a deliberate rejection of cash as a long term store of value.

Balance sheet diversification with asymmetric upside

BTC is treated as a long duration, scarce asset that can protect purchasing power as fiat weakens. In portfolio terms, BTC can offset the slow decay of cash and low real yields over time. The bet is simple: if BTC trends up over years, the company’s balance sheet becomes stronger without needing operational growth.

The operating objective

The job is not just to own Bitcoin. The job is to grow BTC per share through the cycle, while avoiding forced selling and avoiding value destructive dilution.

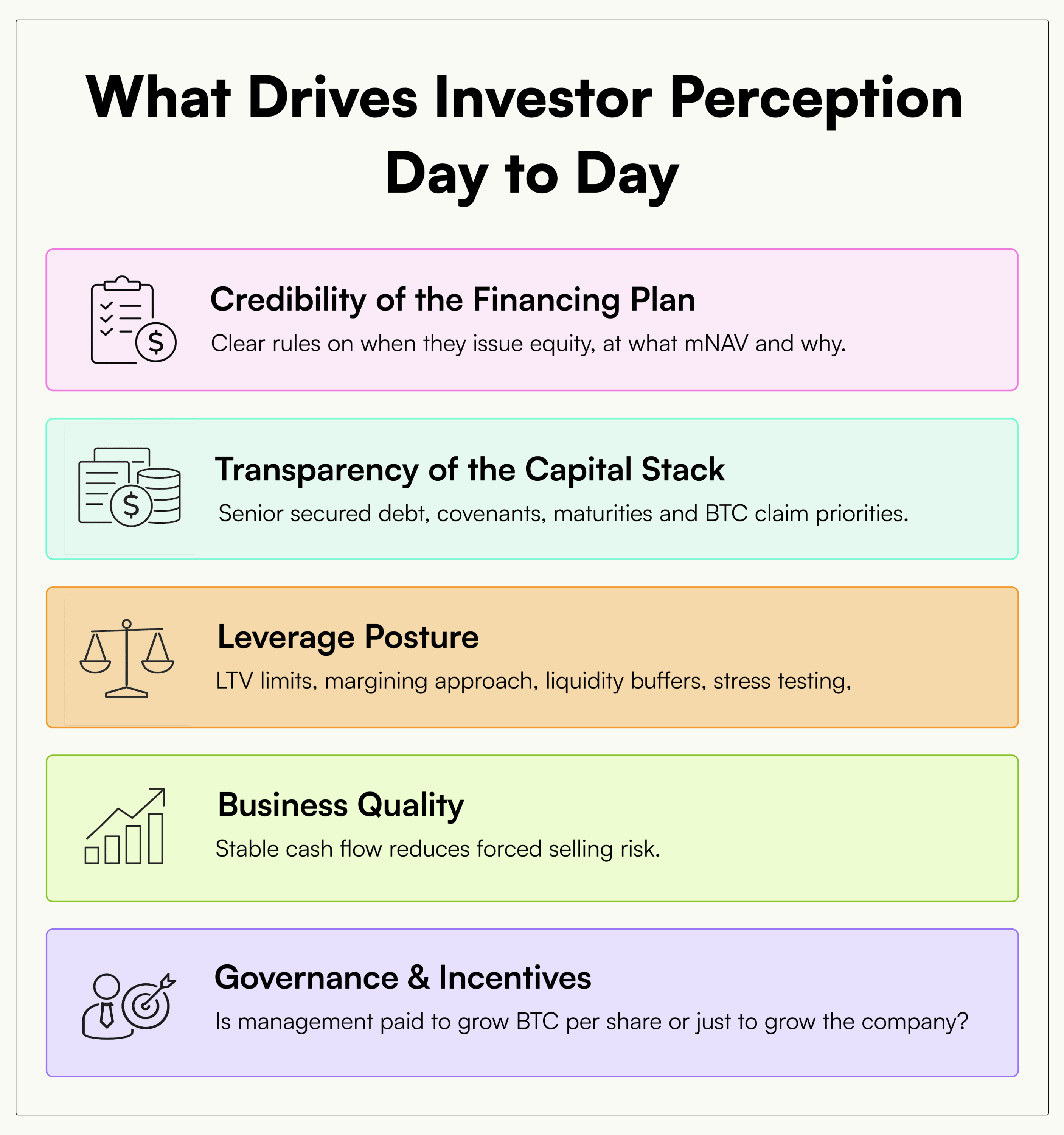

The single most important metric: BTC per share

Definition: total BTC attributable to common shareholders divided by fully diluted shares outstanding.

Why it matters: you can grow headline BTC and still destroy per share value if you issue stock too cheaply or take on senior debt that effectively claims the BTC.

What success looks like:

- BTC per share trend: up over multi year period (up and to the right)

- mNAV discount or premium: premiums matter because they make equity issuance accretive, chronic discounts make growth harder

- Funding discipline: equity issuance only makes sense if it increases BTC per share

Unencumbered BTC and a clear lien stack. Investors need to know what portion of BTC is truly free and clear, and what sits above it

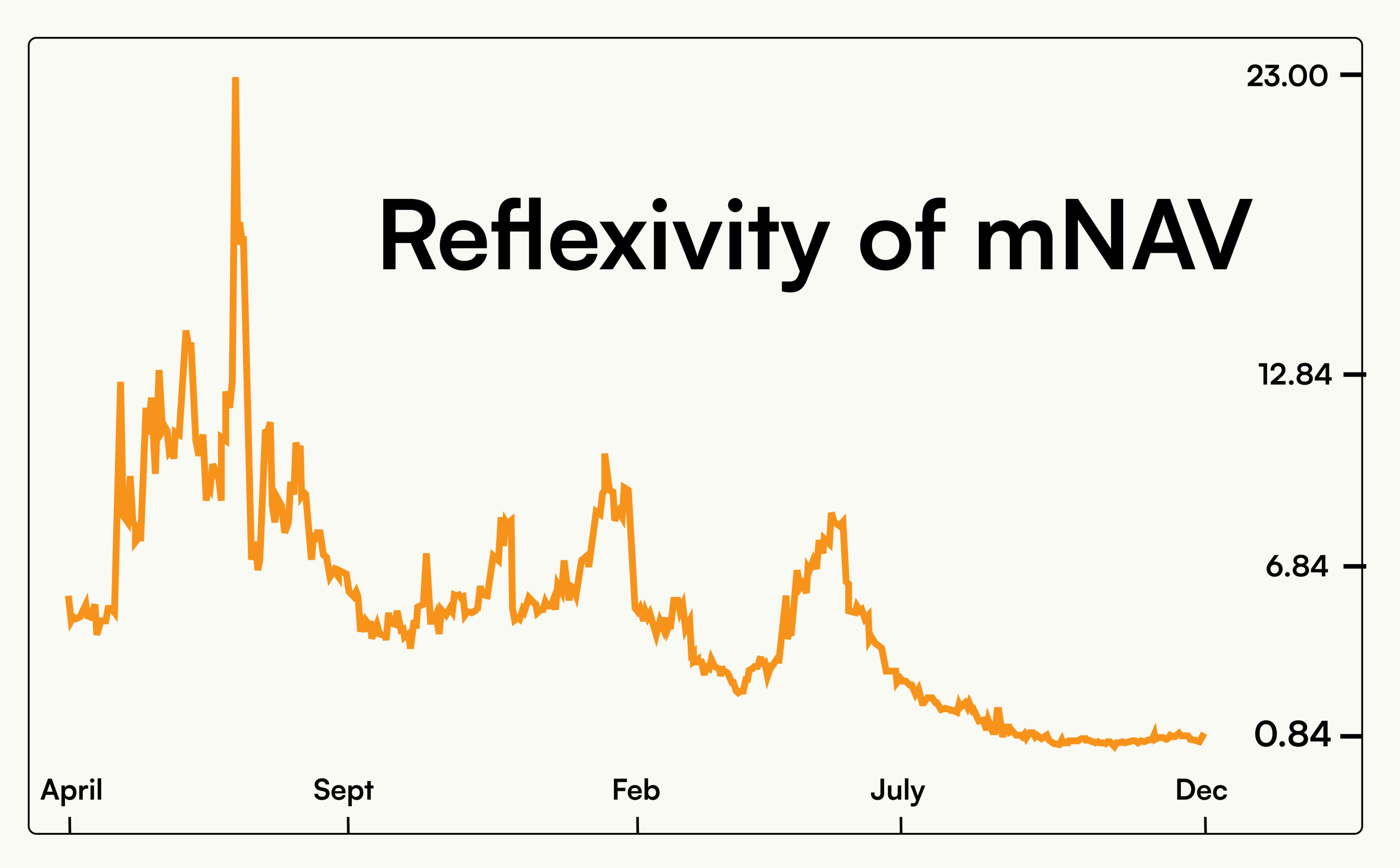

mNAV, and why it is reflexive

mNAV is the market’s opinion about the wrapper around the Bitcoin.

Definition in this piece: market cap divided by the market value of its BTC holding. Some analysts use enterprise value over BTC value. This uses market cap over BTC value for simplicity.

- mNAV > 1: the market is paying a premium to access the structure and its ability to compound BTC per share

mNAV < 1: the market discounts the structure, usually due to liquidity, leverage, governance, dilution risk, or weak operating fundamentals

mNAV can swing a lot because it is not an intrinsic property of the Bitcoin held. It is a market opinion about the wrapper that sits around that Bitcoin. The equity is a leveraged claim on strategy, not just BTC. Investors price governance, funding plans and downside risk. A DAT can hold the same BTC as another and trade at a very different mNAV because the market trusts one structure and distrusts the other.

Liquidity and positioning amplify moves. Small floats, crowded trades and wide spreads can cause mNAV to overshoot in both directions.

mNAV is reflexive because it feeds back into what the DAT can do next, which then changes mNAV again.

Premium loop (mNAV above 1)

Investor confidence rises, the stock trades rich to mNAV. The company can issue equity at a premium and buy BTC. If issuance is done correctly, BTC per share increases. That validates the strategy and reinforces the premium.

Discount loop (mNAV below 1)

Confidence drops, the stock trades below mNAV. Equity issuance becomes dilutive, so growth stalls. Funding costs rise, or management reaches for riskier leverage. Investors price higher downside, and the discount persists or widens.

mNAV moves violently because it is not just a measure of Bitcoin. It is a measure of trust.

Different types of DATs

Bitcoin DATs are not one uniform category. There are many variations in mandate, capital structure, and operating quality. But 2025 was largely defined by two dominant archetypes that the market repeatedly rewarded and then repriced: the long term builders that compound through cycles, and the fast pivots that chased the premium trade.

A) Missionary DATs (Pure-Plays that build through cycles)

Missionaries is an informal label. It refers to an explicit long term Bitcoin treasury mandate, BTC per share focus, and a public commitment that implies a low probability of discretionary selling.

Think….

- Strategy (MSTR)

- Metaplanet (3350 TSE, MTPLF OTC)

- Semler Scientific (SMLR)

B) Mercenary DATs (copy trade)

Mercenaries is also an informal label. These are listed companies that were already in structural decline, adopted a Bitcoin treasury policy at the peak of category enthusiasm in the summer of 2025 and temporarily rode an mNAV premium to revive their stock. They are not Bitcoin first businesses. They are public market shells chasing narrative alpha.

How to spot one, a simple test:

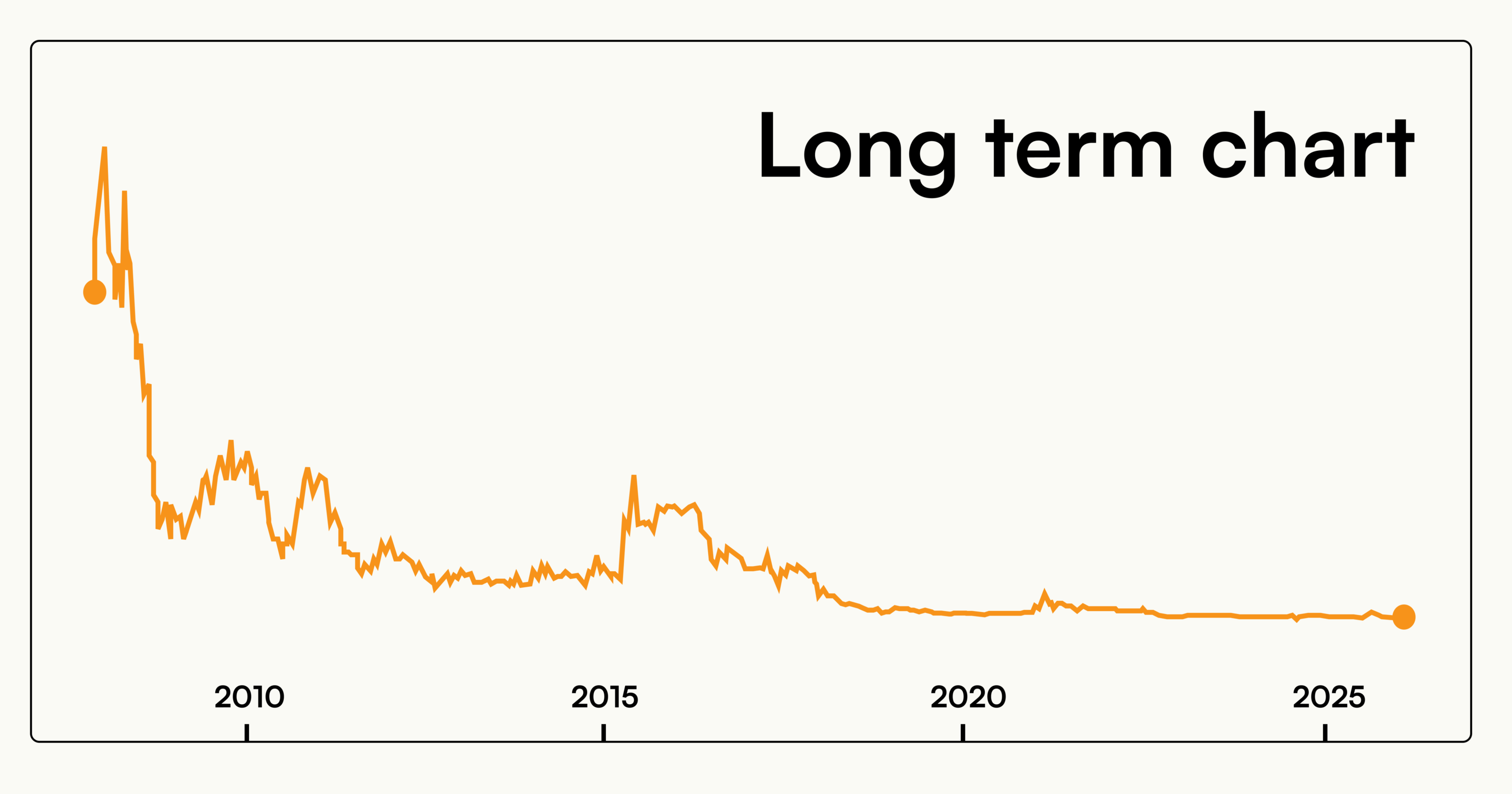

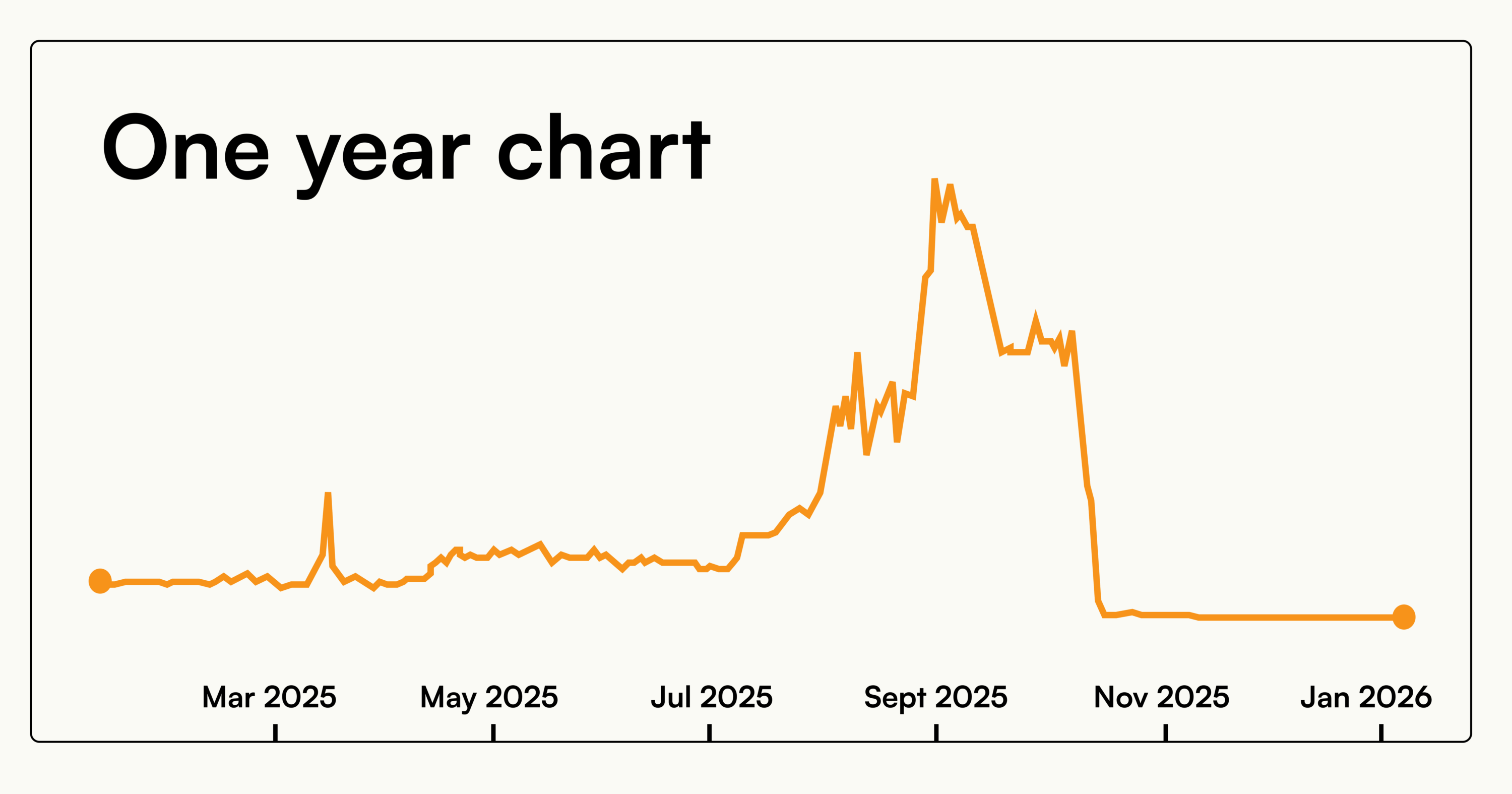

- Long term chart: years of decline

- One year chart: a sharp 5 – 10x spike immediately following a Bitcoin treasury pivot announcement, typically the summer of 2025

- Current price: a retrace that erases most of the move, confirming the narrative outran fundamentals of the business and its Bitcoin strategy

These firms typically:

- Announced “Bitcoin adoption” when the category premium was peaking

- Have weak or non existent operating cash flow

- Issued new equity during or after the pump

- Hold trivial BTC amounts relative to market cap

- Offer limited disclosure on custody, leverage, or treasury policy

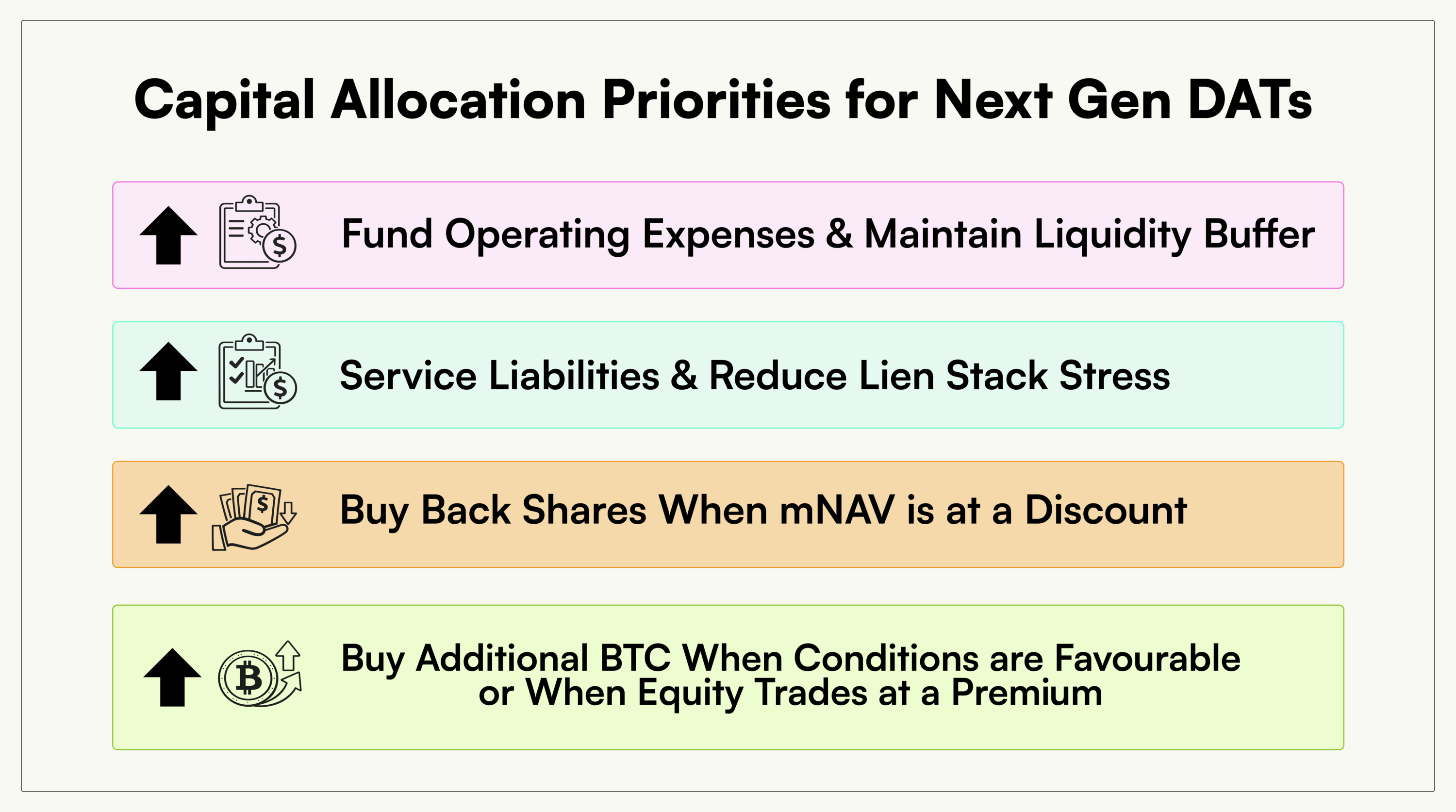

When the premium disappears, the strategy breaks. Equity issuance turns dilutive, funding dries up and these firms face a hard choice. Many will either sell part or all of their BTC to fund operations or repay liabilities, or consolidate into larger vehicles that can survive without constant dilution. That washout is healthy. It clears noise and leaves space for missionary grade DATs that can compound BTC per share with discipline and transparency.

How they fund BTC buys, and why the ATM regime is breaking

Bitcoin DATs executed aggressive capital raising strategies throughout 2025. Total financing exceeded $29 billion, more than double 2024, with most deals structured as private placements, ATM issuance and financed through a sophisticated mix of capital structures such as convertibles, loans, credit lines.

Bitcoin DATs are not one model. Some are missionary vehicles built to compound BTC per share through cycles with disciplined financing and a low tolerance for forced selling. Others are mercenary pivots, often legacy businesses in decline that adopted a Bitcoin treasury during the 2025 mNAV premium frenzy to revive a fading stock, then retraced once fundamentals reasserted. Most still rely on capital markets, equity issuance and BTC backed borrowing, while a growing minority are starting to behave more like allocators, adding selective yield, revenue sleeves, or using operating cash flows to create BTC purchasing power when mNAV premiums disappear.

Most DATs use public markets to raise capital, then convert that capital into BTC. This works best when the stock trades at a premium to BTC NAV (mNAV > 1).

Common tools include:

- ATM programs

- Bought deals and placings

- Convertible notes

- Preferred or structured equity

The ATM led model compounds only while the equity trades at a sustained mNAV premium. Once the stock slips below 1.0, issuance flips from accretive to dilutive and the primary engine of BTC per share growth shuts down. The category has now seen this dynamic play out in real time. A growing share of DATs trade at discounts, which means the sector cannot rely on ATMs as the default purchasing program.

When it works: at a premium, investors are paying more than a dollar for a dollar of Bitcoin exposure through the wrapper. Issuance can be accretive and BTC per share can rise.

When it fails: at a discount, the market values your Bitcoin at less than a dollar through the wrapper. Issuing shares to buy BTC at spot is dilution.

Common problems in the current evolution of DATs

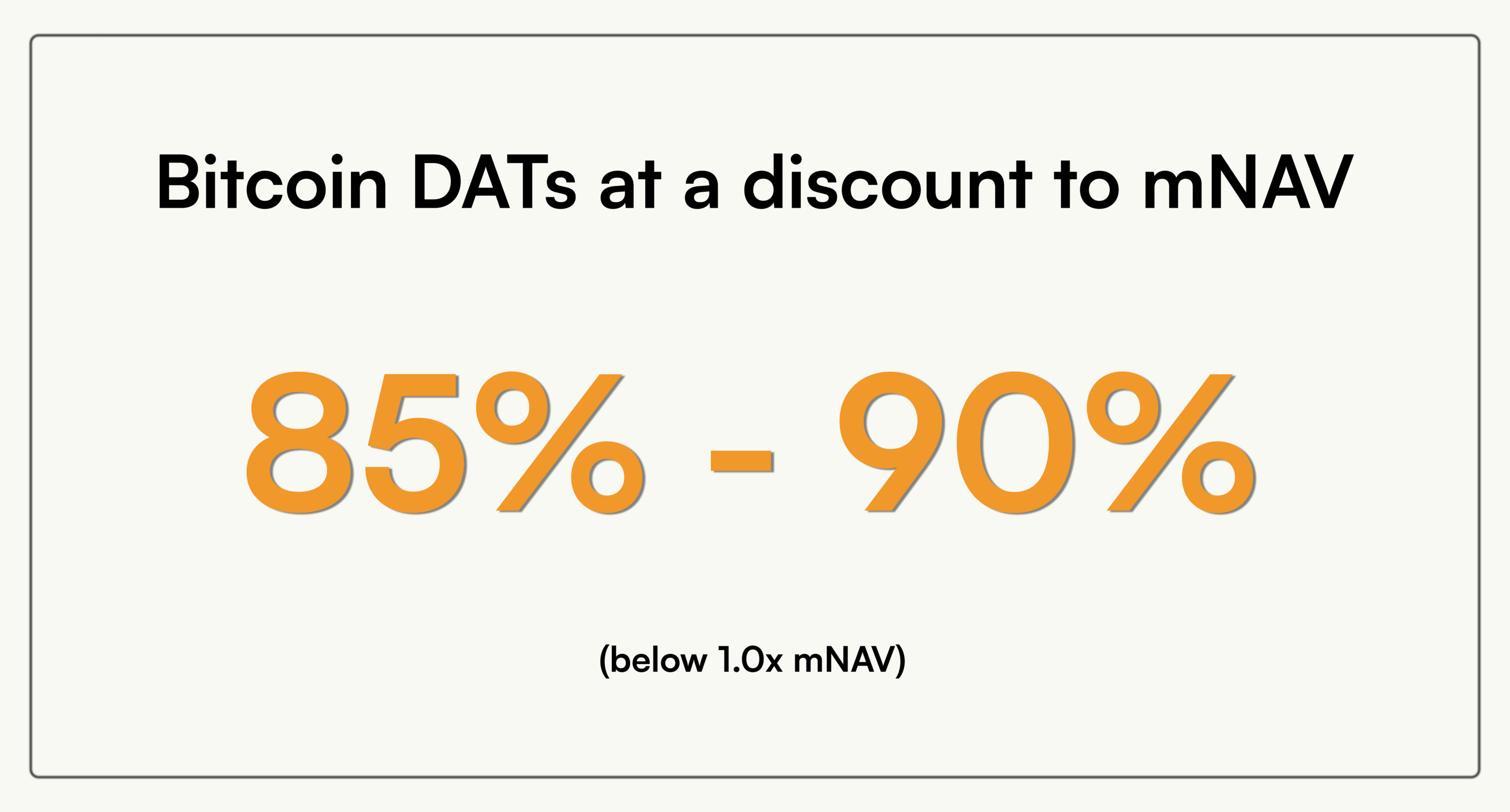

Most DATs lack a durable engine to increase BTC per share without relying on non-dilutive capital. Before the early February sell off, nearly 40% were trading below 1.0x mNAV, where the issuance flywheel reverses. Today, with BTC around $67k, that figure has risen to 85-90% of companies.

BTC is not productive on its own. If you just hold it, your only growth comes from price appreciation, not BTC per share accretion. Meanwhile, a listed DAT has real carrying costs: custody and safekeeping, audit and reporting, listing and compliance and operating expenses. If it cannot fund OpEx from cash flows, it eventually funds itself by issuing equity or selling BTC, both of which work against BTC per share.

To grow BTC per share you need cheap capital (equity at an mNAV premium) or cash flows or low risk BTC denominated yield. When mNAV drops below 1, equity is no longer cheap, it becomes dilutive. That is when DATs reach for leverage, complex yield, or opaque financing to keep the story alive, and those choices produce some of the failures investors associate with the category.

The sector is splitting into three mNAV buckets with a shrinking middle:

- Near parity and above: credible scalers

- Grey zone (0.50 to 0.90): outcomes depend on management execution. Good management and well executed policies can reduce the discount back toward parity. If not, the discount is likely to persist and continue slipping.

- Below 0.50: the danger cohort, where the market prices structural failure and liquidation risk

Dilution math is why discounts become traps and ultimately value destructive. At sub 1.0x mNAV, raising equity becomes mathematically value destructive. At 0.75x mNAV, a company that raises $12m must issue shares representing $16.0m of Bitcoin mNAV. Even if every dollar is used to buy BTC, shareholders effectively gave up $16.0m of NAV to acquire $12m, a 25% per share hit. Repeated sub 1 raises create a destructive loop, dilution lowers BTC per share, confidence falls, and the discount deepens. What begins at 0.75x becomes 0.70x after dilutive raises, then 0.65x as confidence evaporates.

Leverage and disclosure problems are usually downstream. The core issue is a lack of BTC purchasing power that is non dilutive. Premiums make issuance accretive and support BTC per share growth. Discounts flip the math, stall the engine, and push weaker DATs toward riskier fixes.

The next evolution of DATs, active BTC asset managers

2025 proved that public “Bitcoin treasury companies” can accelerate corporate adoption, but the next wave may come from ordinary businesses that add Bitcoin to the balance sheet without reinventing their identity around it. Corporate Bitcoin ownership does not need to be a proxy trade. Companies can hold it for the same reasons individuals do: diversification, long term store of value, upside exposure, and permissionless money, including use cases in cross border payments.

Beyond this, the next evolution of DATs is simple: going a step further than just holding BTC, they stop being passive BTC holders and become active BTC asset managers, using risk controlled yield and revenue generated from their BTC holdings to create a durable source of BTC purchasing power through cycles.

The market has learned that the pure ATM then buy BTC playbook is not a durable compounding engine for most treasuries. The next phase is more likely to be defined by consolidation and experimentation with models that create BTC purchasing power without constant dilution. Expect a split between companies that merely hold Bitcoin as a treasury asset and Bitcoin companies that generate cash flows and recycle that revenue into a disciplined BTC purchasing program. In parallel, more treasuries will move toward active management of their BTC stack, monetising it in controlled ways to fund costs and accretive actions through cycles.

Cashflows and yield matters because it fixes the core structural problem:

- It creates an internal funding source not dependent on equity markets

- It reduces the need to issue stock and dilute shareholders, particularly in drawdowns

- It can support BTC per share accretion when equity issuance would be dilutive

The key use case is buybacks at a discount. When a DAT trades at mNAV < 1, issuing equity destroys BTC per share. Buying back shares at a discount can be highly accretive. Yield provides cash flow to do this without selling core BTC. At a discount, the best investment is often your own equity.

How Rootstock is helping DATs

DATs need BTC purchasing power through cycles that does not rely on issuing equity at a premium. They still have unavoidable carrying costs, so passive holding is not operationally free. The next step is to monetise a portion of the BTC stack in a way that is transparent, risk controlled, and institutionally credible.

Rootstock’s role is to help DATs explore how to move from passive BTC holding to institutional grade BTC monetisation including:

- BTC denominated yield rails via an institutional oriented vault frameworks

- Transparency by default with on chain verification and reporting

- Institutional infrastructure and controls such as MPC workflows and policy guardrails

Holding Bitcoin on a corporate balance sheet used to be a radical move. Now the harder question is whether Bitcoin can be treated as productive capital without weakening its role as a long term reserve asset. BTC yield is not about chasing the highest headline number. It is about turning a treasury into repeatable purchasing power, with clarity on value creation versus risk transfer.

Every yield path has trade offs. Counterparty exposure, liquidity constraints, volatility and liquidation risk and governance gaps show up quickly once BTC moves from passive reserve to active deployment. The question is not whether yield exists, it does. The question is whether it can be delivered in a way that is balance sheet led, auditable and designed to minimise tail risk.

Consistency, discipline and framework design will determine which treasury strategies are sustainable and which were just a short term trade. That is why the path matters as much as the yield.

Yield will not be right for every DAT, and some treasuries should remain fully passive by mandate. But every serious allocator has an obligation to understand what is available, the risks and the controls. In public markets, that is part of fiduciary duty.

A new cohort of asset managers is emerging without the same history of simply holding through the last decade. They will face financialisation directly. Accumulate first, then compete by making the asset productive within controlled constraints.

The point is not to force one strategy. It is to offer a controlled path from passive holding to disciplined monetisation, sized and governed to match each DAT’s mandate.

Rootstock is a Bitcoin secured execution environment through merge mining, and rBTC is designed to remain 1:1 pegged with BTC through the PowPeg mechanism. The institutional pitch is that yield should be structured on execution layers with auditability, policy controls and clear custody workflows, not opaque balance sheet promises.

Closing thoughts

Bitcoin DATs are not all the same. At their best, they are disciplined balance sheet strategies built around one scoreboard, BTC per share. At their worst, they are weak listed companies using Bitcoin as a narrative patch. The hard constraint is not Bitcoin volatility, it is capital structure. Most DATs do not have durable, non-dilutive BTC purchasing power. They depend on an mNAV premium driven issuance flywheel, and the market has now seen how fragile that is.

That dynamic is forcing a split. Near parity and above sit the credible scalers. In the 0.50 to 0.90 grey zone, outcomes are binary. Below 0.50, the market is no longer debating valuation, it is pricing a high probability of restructuring or eventual BTC liquidation.

If you are underwriting a DAT, stop underwriting the headline BTC number. Underwrite the engine. Demand transparency on BTC per share, issuance rules, the capital stack and lien priority, leverage limits and buffers, liquidity planning and the plan to fund OpEx without selling the treasury. Back the structures that can compound BTC per share through a full cycle without hiding risk in leverage or dilution.