As Kamina Bashir from BeInCrypto recently reported, public bitcoin miners sold a record 32,000+ BTC in the first quarter of 2026. But that does that mean they’ve lost faith in BTC as an asset?

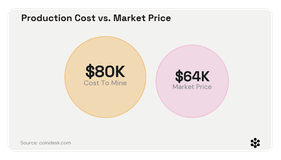

In many cases the answer is no, it was simply liquidity management. With the weighted-average cash cost to mine a coin sitting near $80k and hashprice compressed to roughly $28–30 per PH/s/day, operators were offloading inventory close to production cost just to keep the lights.

A smaller subset of these miners, as our institutional team recently discussed, did this to fund a pivot into AI compute.

While at first glance this may seem to make business sense, selling near a ~$80K cash cost into a ~$64K market is probably one of the most expensive ways to raise a dollar.

Selling BTC near a cyclical low crystallizes the loss, surrenders the upside, and triggers a taxable event. For a CFO, it is the financing decision you least want to be forced into, made at exactly the wrong moment.

Join our upcoming webinar on Bitcoin-secured lending. Save your seat →

And it is no longer just the miners. In late May, Strategy, the flagbearer of “never sell your bitcoin” confirmed its first Bitcoin sale since 2022 with further sales under a new capital framework to fund reserves, dividends and buybacks. When the most committed holder in the market reverses a “diamond hands” doctrine and builds selling into its playbook, every treasury team should be re-examining the alternatives to liquidation.

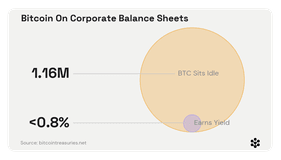

There is a structural reason this keeps happening. Roughly 1.16 million BTC now sits on corporate balance sheets, and the overwhelming majority of it earns nothing. It is the single largest pool of pristine, liquid collateral in the world, parked as a static reserve asset. When a funding need arrives, the instinct is to sell, because the machinery to borrow against Bitcoin has only recently matured to what would be considered an institutional-grade level.

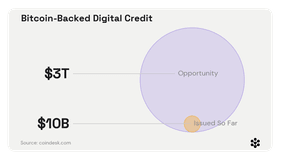

But that machinery is now arriving fast. Bitcoin-backed “digital credit” issuance reached roughly $10 billion in under a year, one of the quickest product launches capital markets has seen, and at Consensus in May, treasury executives framed the long-term prize as a $3 trillion market, the implied size of even a 1% Bitcoin allocation against the $300 trillion global credit market. Bitcoin-native lenders have already originated over a billion dollars in loans against custodied BTC. The plumbing for treating Bitcoin as collateral, rather than inventory to be liquidated, is being built in real time.

That is precisely the decision our latest webinar is built to unpack.

Bitcoin as Collateral: Exploring Bitcoin-Collateralized Lending and the Institutional Opportunity In 60 minutes the RootstockLabs Institutional team joined by a number of partners in the space cover the real trade-offs between holding, selling and borrowing against BTC; the mechanics that actually matter — optimal LTV, collateral management and liquidation dynamics; and case studies of how miners, treasury companies and Bitcoin-native operators are approaching liquidity planning today.

If you run a balance sheet with Bitcoin on it, the question isn’t whether to think about this. It’s whether you do so before the next funding need forces your hand.

For eligible institutional or qualified counterparties only.